| HEADLINE |

|

The poor pay highest price

Bangladesh tops Asia in mobile cash-out charges

No other country in Asia makes people pay as much as Bangladesh does to withdraw their own money. Mobile Financial Service (MFS) charges here are up to 15 times higher than bank rates, and with no regulatory cap from Bangladesh Bank (BB), operators set prices freely while users bear the cost.

No other country in Asia makes people pay as much as Bangladesh does to withdraw their own money. Mobile Financial Service (MFS) charges here are up to 15 times higher than bank rates, and with no regulatory cap from Bangladesh Bank (BB), operators set prices freely while users bear the cost.The system bleeds low-income users as regulators defend rules that leave room for abuse--a silence that works like a license.

The BB has laid out broad policy guidelines for MFSs but has never fixed a ceiling on cash-out charges. That single gap has opened the floodgates. Operators are free to set their own rates, and customers carry the burden.

A senior BB official admitted, "We monitor for irregularities, but there is no fixed cap on what providers can charge. We try to balance innovation and inclusion."

Transparency Inter-national Bangladesh (TIB) Executive Director Dr Iftekharuzzaman said withdrawing Tk25,000 through leading MFSs costs between Tk400 and Tk460, while banks charge just Tk30 for the same amount.

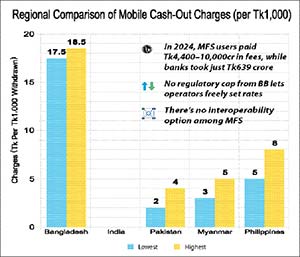

"This is one of the highest rates in Asia," he warned. He called the rules unbalanced and the impact discriminatory, noting that day labourers, rickshaw-pullers, and garment workers pay Tk17.50 to Tk18.50 per Tk1,000, a silent poverty tax disguised as a convenience fee.

Even Nagad's reduced Tk9.99 per Tk1,000 has restrictions that keep most users locked out. For millions, the so-called digital revolution is charging entry fees they can't afford.

Iftekharuzzaman said that in 2024 alone, MFS customers paid between Tk4,410 crore and Tk10,197 crore in cash-out fees. Banks, by comparison, collected only Tk639 crore for equivalent withdrawals--a stark gap showing a system tilted toward operators, enabled by a regulator unwilling to impose limits.

He argued this is not competition... it is legalised exploitation. "What they call service charge is, in reality, bleeding the poor."

The legal framework is outdated and unjust. "The policies allow discriminatory rates," Iftekharuzzaman said. "Millions of low-income people are being forced to pay unfairly. We need a legal ceiling on charges and stronger protection for customers."

A garment worker sending money home or a rickshaw-puller cashing out small amounts pays operators far more than any bank customer. The so-called convenience becomes a trap.

Another senior BB official defended the system, saying providers need "space to recover costs and expand infrastructure." That logic may sound technical but misses the human cost. No other sector allows operators to charge 15 times the benchmark without scrutiny. Here, weak rules have turned into a legalised drain on the poor. In India, mobile money cash-outs are free. In Pakistan, the charges are far lower. In Myanmar, rates remain modest. Against that backdrop, Bangladesh sits at the top of the price ladder--the costliest place in Asia to cash out your own earnings.

The irony bites deeper because Bangladesh is often praised as a pioneer of digital financial inclusion. Yet, instead of inclusion at low cost, the country has created a model of inclusion at high price. What should have been empowerment has turned into extraction.

Bangladesh Competition Commission (BCC) member Md Akhteruzzaman Talukder admitted that three operators dominate the market but said no formal complaint or evidence of collusion has reached his desk.

"We act on complaints or on visible syndication," he explained. "So far, neither has been presented."

That means the commission is silent while customers pay the highest charges in Asia. The BCC member noted that if monopoly abuse is proven, the commission can investigate and punish--but until then, it waits. That wait is costly for millions scraping through small withdrawals.

Another senior BB official in the Payment Systems Department (PSD) said: "We do not want to stifle innovation by fixing every fee. But we are reviewing the structures." The review has been pending for years. In the meantime, billions drain from pockets that can least afford it.

Information technology expert Fida Haq said the charges are exorbitant and contradict the government's financial inclusion policy. He urged for laws to lower them. He added that BB should not turn a blind eye to any operator and noted the lack of interoperability among MFSs--a Bkash user, for instance, cannot send money to a Nagad wallet.

To facilitate interoperable transactions, Bangladesh Bank launched Binimoy in November 2022, designed to enable fund transfers across banks, MFSs, and payment service providers. However, the platform failed amid irregularities and was eventually scrapped. Currently, Bkash dominates the market, while Nagad faces regulatory and operational hurdles. Experts say this imbalance fosters monopolistic conditions that exploit users.

When contacted a senior bKash official requesting anonymity said, "Not all of our customers pay Tk18.50 for cashing out.

"We have different options. So people can choose the most affordable on e for them. Customers who set up a Priyo Agent can cash out up to Tk25,000 each month at Tk14.90 per thousand. Beyond that limit or at non-Priyo agents, the standard rate of Tk18.50 applies."

The contradiction is sharp, the injustice plain, and the silence deafening. Unless capped and corrected, Bangladesh's proud digital finance journey risks being remembered not for empowerment - but for exploitation at scale.

Loading...

Loading...

Also read

Editor : Iqbal Sobhan Chowdhury

Published by the Editor on behalf of the Observer Ltd. from Globe Printers, 24/A, New Eskaton Road, Ramna, Dhaka.

Editorial, News and Commercial Offices : Aziz Bhaban (2nd floor), 93, Motijheel C/A, Dhaka-1000.

Phone: PABX- 41053001-06; Online: 41053014; 01550707296 Advertisement: 41053012; 01550707291

E-mail: [email protected] [email protected]

Published by the Editor on behalf of the Observer Ltd. from Globe Printers, 24/A, New Eskaton Road, Ramna, Dhaka.

Editorial, News and Commercial Offices : Aziz Bhaban (2nd floor), 93, Motijheel C/A, Dhaka-1000.

Phone: PABX- 41053001-06; Online: 41053014; 01550707296 Advertisement: 41053012; 01550707291

E-mail: [email protected] [email protected]